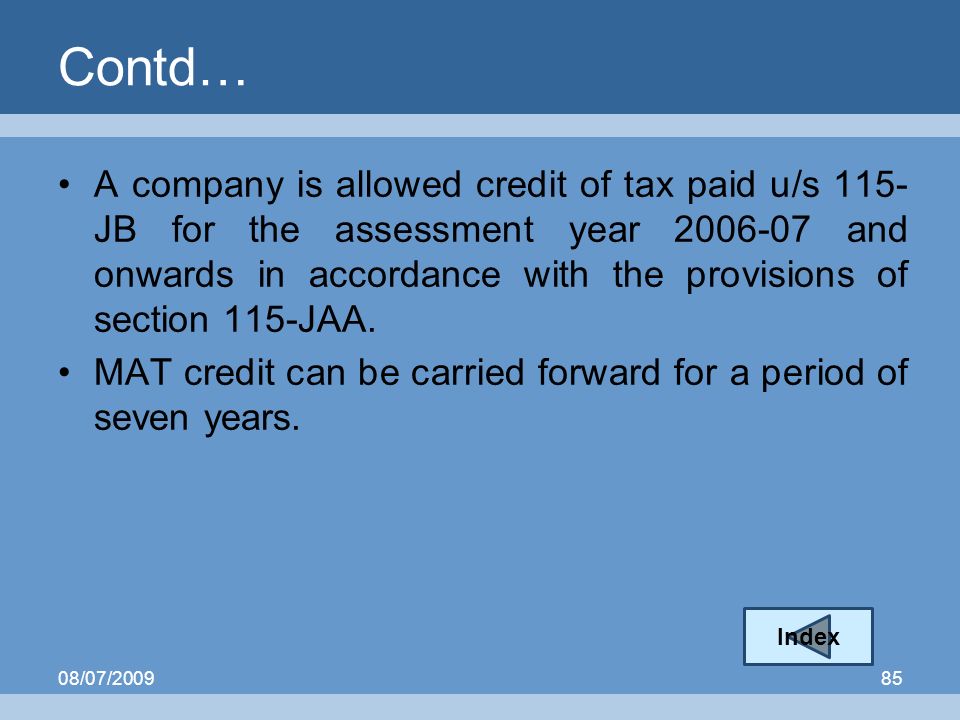

Mat Credit Entitlement Period

Mat Credit Whether Credit For Surcharge And Education Cess On Brought Forward Mat Credit Is Available The Tax Talk

Surcharge And Cess Is To Be Calculated After Deducting Mat Credit U S 115jaa From Tax On Assessed Income

Guide To Minimum Alternate Tax For Ind As Compliant Companies

The Bane Of Mat Credit

Budget 2017 Timeline To Claim Mat Credit Enhanced To 15 Years Business News The Indian Express

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

The asset may be reflected as mat credit entitlement.

Mat credit entitlement period.

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Standalone Financial Statements Mindtree

Prakash Industries Ltd Prakash Stock Opportunities Valuepickr Forum

Firms Opting For Lower Tax Regime Can T Adjust Accumulated Credits On Mat Business Standard News

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Now Through April 20th 2015 Tax Relief Event Get A Discount Equal To Double Your Sales Tax Or 60 Months No Interest Ashley Furniture Richland At Home Store

Minimum Alternate Tax Mat Section 115jb

Significant Accounting Policies And Notes To The Accounts For The Year Ended March 31 2013 Mindtree

Consolidated Financial Statements Mindtree

Racl Geartech Limited Stock Opportunities Valuepickr Forum

Mat Vs Amt Minimum Alternate Tax Alternate Minimum Tax Indiafilings

What Is Minimum Alternate Tax Mat News Budget 2020 News Mat Calculation

Https Www Dishmangroup Com Files Dishmangroup Investor Relations Carbogen 20amcis 20 India 20ltd Pdf

Sutlej Textiles Industries Fundamental Analysis Dr Vijay Malik

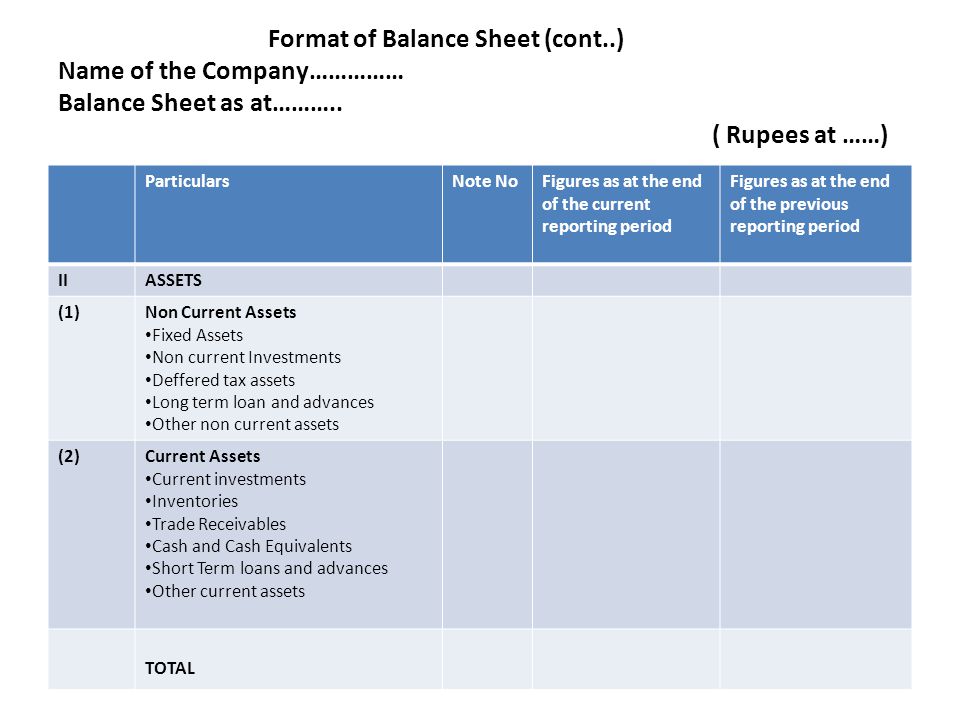

Balance Sheet As Per Companies Act Ppt Video Online Download

Consolidated Financial Statements Mindtree

Copilul Tau In Rolul Principal Atelier De Teatru In Engleza Expressions Blog Workshop

Income Tax A Y Index 1 Introductionintroduction 2 Residential Statusresidential Status 3 Tax Ratestax Rates 4 Income From Salaryincome Ppt Download

Common Size Trend Analysis Of Financial St Of Pharma Co

Mat Credit Forward Limit Increased Income Tax Budget Changes 2017

Http Prakash Com Pdfs Pil Results 31032k18 Pdf

Datamatics Global Services Ltd Fundamental Analysis Dr Vijay Malik

What Is Budget Budget The Statement Of The Estimated Receipts And Expenditure Of The Provincial Government For A Fiscal Year Which The Provincial Government Ppt Download

Sharda Motor Industries Ltd Fundamental Analysis Dr Vijay Malik

Source : pinterest.com